Creator Economy Statistics 2026: Market Size, Earnings & Growth (100+ Data Points)

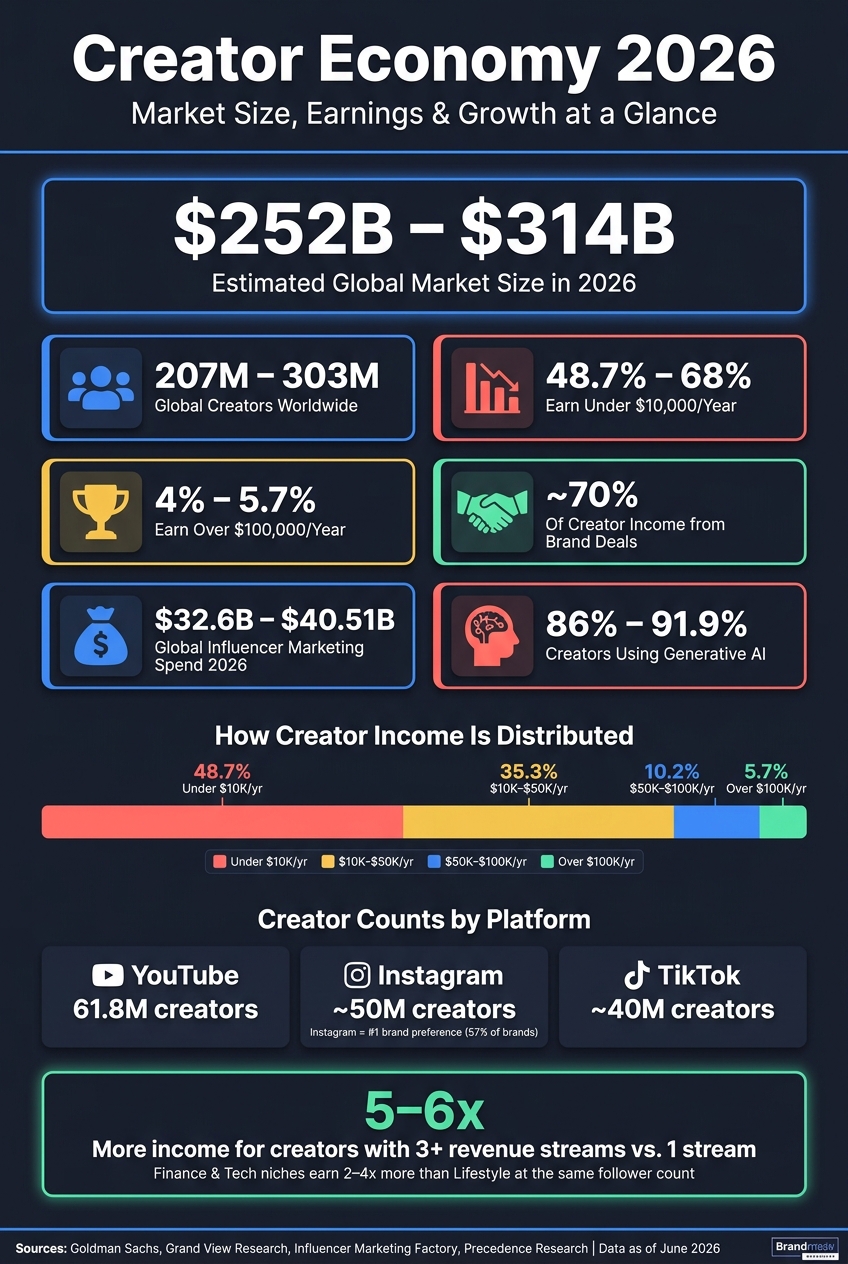

Massive creator-economy growth with uneven pay: $252–$314B market, 207–303M creators, rising brand spend and 86–92% AI use.

Massive creator-economy growth with uneven pay: $252–$314B market, 207–303M creators, rising brand spend and 86–92% AI use.

4.98 /5 - from 58k reviews

Trusted by 50,000+ creators — get real engagement delivered to your profile in minutes, not days.

The short answer: in 2026, the creator economy sits at about $252 billion to $314 billion, but most creators are not making huge money. At the same time, brand spend keeps climbing, and AI use is now common.

If you want the big picture fast, here it is:

What this tells me is simple: the market is getting bigger, but income is still stacked at the top. More people are making content, more brands are spending, and more work is being done with AI. But for most creators, money still comes down to niche, audience response, and having more than one income stream.

Creator Economy 2026: Key Stats at a Glance

| Area | 2026 Snapshot |

|---|---|

| Market size | $252B–$314B |

| Global creators | 207M–303M |

| Earn under $10,000/year | 48.7%–68% |

| Earn over $100,000/year | 4%–5.7% |

| Brand deals share of income | ~70% |

| Influencer marketing spend | $32.6B–$40.51B |

| AI adoption | 86%–91.9% |

| Brand-favorite platform | |

| Largest creator base | YouTube |

| Top income platform by creator share | TikTok |

While TikTok leads in creator share, many still monetize their Instagram accounts to diversify earnings. |

So if you’re reading this to understand where the creator economy stands in June 2026, the answer is: big market, fast growth, uneven pay, and heavy brand and AI influence.

The creator economy is worth roughly $250 billion to $323 billion in 2026, depending on what a given study counts. Some reports look at direct creator income, such as monetizing an Instagram presence. Others look at the full ecosystem around creators, like platforms, software, ad spend, commerce, agencies, and investor activity.

That’s why the numbers don’t line up perfectly. The best way to read them is source by source.

These estimates vary because each firm is measuring a different slice of the market. Here’s how the main 2025–2026 figures compare.

| Source | Reported Market Size | Forecast Year | Projected Size | What the Estimate Includes |

|---|---|---|---|---|

| Goldman Sachs Research | ~$300B | 2027 | $480B | Broad TAM: ad spend, commerce, and creator tools |

| Grand View Research | $310.4B | 2033 | $1,345.5B | Broad ecosystem: platforms, tools, and brand spend |

| Precedence Research | $313.95B | 2035 | $2,084.6B | Broad ecosystem valuation |

| Research and Markets | $323.48B | - | - | Unspecified broad market estimate |

| Research Nester | $214.4B | 2035 | $1,350B+ | Direct creator revenue only |

| DataM Intelligence | $254B (2025 est.) | 2032 | $894.8B | Direct creator revenue plus platform revenue |

The gap comes down to scope. Narrower studies count direct creator earnings. Broader ones pull in platforms, tools, agencies, commerce, and investment too.

So averaging all of these into one neat figure doesn’t help much. It’s better to ask a simpler question: what layer of the market is this source measuring? That gives you a much cleaner read on the data.

Once that 2026 range is on the table, the next thing to look at is growth.

The market passed $250 billion in 2025 and is still growing fast. Depending on the slice being measured, CAGR estimates range from about 10% to 23.3%. On the ad side, creator economy spend is growing about 4x faster than the total media industry - 26% year over year versus about 6.5%.

| Year | Market Size (Est.) | Source | Notes |

|---|---|---|---|

| 2024 | $205.25B | Research and Markets | Baseline for current growth models |

| 2025 | $250B–$254.4B | Goldman Sachs / Precedence | Crossed the quarter-trillion mark |

| 2026 | $313.95B–$323.48B | Precedence Research / Research and Markets | Current headline valuation range |

| 2027 | $480B | Goldman Sachs | Projected TAM estimate |

| 2030 | $500B+ | Multiple sources | Long-term projection |

| 2033 | $1,345.5B | Grand View Research | Forecast based on 23.3% CAGR |

These figures are not additive. Each source is looking at a different market layer, so stacking them together would give the wrong picture. That fast growth also helps explain a strange tension in the space: the market keeps getting bigger, but creator income is still spread very unevenly. Next comes the number of people creating inside it.

Worldwide creator counts range from 207 million to 303 million in 2026. That gap comes down to one simple thing: different groups mean different things when they say creator.

On the broad end, Linktree and Statista put the global creator population at 207 million. That view includes active creators earning revenue in some form. Goldman Sachs takes a tighter view and puts the professional and semi-professional group at 50 million+.

| Source | Year | Definition Used | Estimated Number of Creators |

|---|---|---|---|

| Linktree / Statista | 2026 | Broad - active creators earning any revenue | 207 million |

| Goldman Sachs / SQ Magazine | 2026 | Narrow - professional / semi-professional | 50 million+ |

Put another way, about 1 in 40 people globally now identifies as a creator.

Even full-time creator doesn't have one fixed meaning across surveys. 46.7% of creators say they are full-time. At the same time, 70% spend 10 hours or fewer per week making content.

That tells you something important: labels can sound neat, but the day-to-day work behind them can look very different.

There’s also a large group between hobbyists and top-tier influencers. About 60 million creators with 5,000 to 500,000 followers are often grouped into the creator middle class.

Raw creator counts don't tell you where the money is. YouTube has the biggest creator base at about 61.8 million creators, followed by Instagram at roughly 50 million and TikTok at around 40 million.

| Platform | Estimated Creator Population | Primary Income Channel (% of Creators) | Brand Preference / Demand | Source |

|---|---|---|---|---|

| YouTube | 61.8M | 34.1% | 37% of brands | Social Blade / Influencer Marketing Factory |

| ~50M | 16.0% | 57% of brands - highest | Fungies.io / Influencer Marketing Factory | |

| TikTok | ~40M | 37.8% - highest | 52% of brands | Fungies.io / Influencer Marketing Factory |

| Twitch | ~9M | N/A | 15% of brands | Fungies.io |

A few patterns stand out fast.

So yes, audience size matters. But where creators earn, and where brands spend, can look very different. Platform reach is only part of the story; the next section shows how uneven creator earnings are.

Big market numbers tell one story. Creator pay tells another.

For most people, earnings land far below the flashy screenshots and viral “I made $1 million in a month” posts. In fact, 48.7% earn under $10,000 a year, while only 4% to 5.7% earn $100,000+.

Creator income is heavily concentrated at the top. A small slice of people takes home a large share of the money, while a much larger group sits in the middle. Roughly 45.6% of creators earn between $10,000 and $100,000 annually. That's the creator middle class.

| Income Band | Share of Creators | Source | Year | Notes |

|---|---|---|---|---|

| Under $10,000 | 48.7% | Influencer Marketing Factory | 2026 | Includes hobbyists and side-income creators |

| $10,000 – $50,000 | 35.3% | Influencer Marketing Factory | 2026 | Combined $10K–$25K (19.2%) and $25K–$50K (16.1%) tiers |

| $50,000 – $100,000 | 10.2% | Influencer Marketing Factory | 2026 | Core full-time earning segment |

| Above $100,000 | 4%–5.7% | Axis Intelligence / Influencer Marketing Factory | 2026 | High-earners ($100K–$250K) and top-tier 2% at $250K+ |

That top-line spread matters because it puts the success stories in context. The median full-time creator earns between $50,000 and $75,000 per year. That's solid income, but it's a long way from the image many people have of creator life.

At the same time, income is moving up for many creators. 51.5% of creators reported higher year-over-year earnings in 2025. So while the odds are still tough, there are signs of steady growth across the space.

The biggest source of money is still brand work. Brand deals account for about 70% of creator income.

"Brand deals account for approximately 70% of total creator income - larger than AdSense, affiliate, merch, and subscriptions combined." - Goldman Sachs

That matters because it shows where the money actually sits. For many creators, the business isn't built on platform checks alone. Platform ad revenue is a primary income source for only 34% of creators. In plain English: YouTube, TikTok, or Instagram may help creators get attention, but brand relationships often pay the bills.

| Revenue Stream | Share / Contribution | Notes |

|---|---|---|

| Brand deals / sponsorships | ~70% of total creator income | Dominant source of creator revenue |

| Platform ad revenue | Primary source for 34% of creators | Important, but secondary to brand deals |

| Affiliate and product income | More than 20% of total creator income | Reflects a shift toward direct creator-to-audience revenue |

Affiliate income and products also play a bigger role now. Together, they make up more than 20% of total creator income. That's a sign that more creators are trying to earn straight from their audience instead of leaning only on sponsors or ad programs.

If there's one pattern that stands out, it's this: creators who earn more usually don't rely on one paycheck.

The clearest predictor of higher earnings isn't follower count. It's income diversification. Creators with three or more revenue streams earn 5–6 times more than those relying on only one source. And creators making $50,000+ per year are much more likely to show up across several platforms, with 78% active on three or more.

Niche also changes the math. Finance and Tech, especially B2B-adjacent categories, outearn lifestyle and entertainment niches by 2–4 times at the same follower count. Same audience size, very different money.

Audience quality matters too. Brands now look past raw follower numbers and focus more on comparing engagement rates and audience quality and authenticity when setting prices. A large audience can look good on paper, but a smaller audience that pays attention often wins.

You can see that in platform-by-platform earnings. On Instagram, creators with 100,000 followers earn an average of $81,700 per year. TikTok creators with the same following earn $44,250 on average. That's nearly double on Instagram, even with equal follower counts.

So the pattern is pretty clear: higher creator earnings tend to come from strong audience quality, better engagement, and a mix of income sources rather than one big number at the top of a profile. That revenue mix also helps explain why influencer marketing spend and AI adoption keep climbing.

Global influencer marketing spend is projected to hit $32.6 billion to $40.51 billion in 2026, up from $32.55 billion in 2025.

| Year | Global Spend | Source | Notes |

|---|---|---|---|

| 2024 | $24.0B | Gigapay / DemandSage | Baseline year |

| 2025 | $32.55B | Influencer Marketing Hub | Milestone year for global growth |

| 2026 (Proj.) | $40.51B | Mordor Intelligence | Projected benchmark |

| 2026 (U.S. only) | $43.9B | IAB | U.S. creator economy ad spend; 18% YoY increase |

That gives you a pretty clear picture: brands are still putting more money into creators, not less.

87% of marketers expect to increase their creator investment budgets in 2026. Instagram branded content still leads brand partnership demand, with 57% of brands choosing it over other channels. TikTok isn't far behind on budget growth either, with 56% of brands increasing their TikTok-specific budgets.

At the same time, smaller creators are getting a bigger share of the pie. Micro and nano-influencers are expected to claim 45.5% of total influencer marketing spend in 2026. That shift matters. It shows that brands don't just want reach. They want trust, tighter communities, and better engagement.

As budgets climb, creators are also leaning on AI to make more content and handle more day-to-day work without doing every task by hand.

AI adoption among creators now ranges from 86% to 91.9%, depending on the study. And it's not a small uptick either. The URLgenius Creator Trend Index found that AI adoption among creators grew 131% year-over-year.

| AI Use Case | Adoption Rate | Source | Year |

|---|---|---|---|

| Multimedia Editing | 24.7% | Influencer Marketing Factory | 2026 |

| Idea Generation | 21.0% | Influencer Marketing Factory | 2026 |

| Script & Caption Writing | 17.2% | Influencer Marketing Factory | 2026 |

| Analytics & Insights | 16.7% | Influencer Marketing Factory | 2026 |

| Automation & Scheduling | 12.3% | Influencer Marketing Factory | 2026 |

The pattern here is simple. Creators are using AI most for the parts of the job that eat up time: editing, brainstorming, writing, reporting, and scheduling.

That time savings adds up. AI cuts manual work by about 15 hours a week, and top users report 2x to 5x higher engagement than creators who don't use it. There's also a pricing shift in the market. Pure AI content is priced 40% to 60% lower than human-made content, while hybrid content - human strategy combined with AI execution - is only 15–30% lower. In plain English, brands may pay less for AI-heavy output, but they still pay more when a real person brings judgment, taste, and audience knowledge to the work.

"The ones who succeed will be those who use [AI] to speed up the work but still trust their own judgment, staying in the driver's seat and leaving AI as a co-pilot." - Alexander Frolov, CEO & Co-Founder, HypeAuditor

The 2026 numbers point in the same direction: more money is entering the market, more platforms are sharing that money, and more creators are using AI as part of their workflow.

Influencer marketing spend is projected between $32.6 billion and $40.51 billion in 2026. Micro and nano-influencers are expected to capture 45.5% of total spend. And 86% to 91.9% of creators are already using at least one AI tool , often leveraging free AI tools to streamline production.

So while the market is getting bigger, it's also getting more split up. More creators are competing for brand dollars. More brands are spreading budgets across Instagram, TikTok, and smaller creator partnerships. And more content is being produced with some level of AI support.

Creator earnings still depend on audience quality. That's the part that doesn't change. Creators monetize best when they have a real, engaged audience. UpGrow helps Instagram creators build that foundation with real followers.

Last updated: June 2026

In 2026, the global creator economy is estimated at $252 billion to $314 billion. That figure covers creator income, platform revenue, brand partnership spending, and infrastructure services.

The range shifts because different analysts draw the lines in different places. Some put the market as high as $480 billion when they count broader commerce and tool spending too.

Even with those gaps, the direction is pretty clear: the market is growing fast. Most forecasts put annual growth at about 22% to 23%, with the creator economy expected to pass $500 billion by 2030.

Pinning down an exact number isn't easy because full-time creator can mean different things depending on the study. Even so, industry research puts the global total at around 50 million professional or semi-professional creators.

In the U.S., Upwork found about 27.7 million independent workers in the full-time creator category in 2024. And among professional creators, about 84.7% post daily or almost every day.

That gives you a sense of the scale here: this isn't a small niche anymore. It's a huge group of people treating content like a job, not just a side hobby.

Estimates change based on the survey and on how each source defines creators. Recent 2026 data puts the share of creators earning more than $100,000 per year at about 5.7% to 5.8%, while other reports put it closer to 4%.

The big picture stays the same: only a small top tier earns at this level, and most creators make far less.

Market-size estimates for the creator economy vary because there’s no single, agreed-upon definition of what counts as creator-driven activity.

Some studies look only at direct creator revenue. Others count the broader ecosystem too, including platform revenue, influencer marketing spend, creator tools, and audience-to-creator transactions.

That gap in scope is the main reason estimates can be so far apart.

The creator economy is moving fast. What used to feel like a niche corner of the internet is now a major part of the global digital economy.

By 2026, estimates place the market between $252 billion and $314 billion. Most analysts also project 20%+ CAGR.

A few forces are pushing that growth:

At the same time, there’s a catch. Earnings are still heavily concentrated among top creators.

Share this post&description=Massive%20creator-economy%20growth%20with%20uneven%20pay%3A%20%24252%E2%80%93%24314B%20market%2C%20207%E2%80%93303M%20creators%2C%20rising%20brand%20spend%20and%2086%E2%80%9392%25%20AI%20use.&image=https://www.upgrow.com/blog-images/assets.seobotai.com/cdn-cgi/image/quality=75,w=1536,h=1024/upgrow.com/6a3c77802902db05ecd7e6f5-1782352425186.jpg)